Is blockchain technology the new internet?

The blockchain is an undeniably ingenious invention – the brainchild of a person or group of people known by the pseudonym, Satoshi Nakamoto. But since then, it has evolved into something greater, and the main question every single person is asking is: What is Blockchain? By allowing digital information to be distributed but not copied, blockchain technology created the backbone of a new type of internet. Originally devised for the digital currency, Bitcoin, the tech community is now finding other potential uses for the technology.

Let’s understand exactly what the blockchain is

Blockchain is a decentralized system for exchange values that uses a shared distributed ledger and ensure transaction immutability achieved by way of blocks & chaining. It Leverages consensus mechanism for validating the transactions and uses cryptography for trust, accountability, security. Blockchain technology comprises four main blocks that can lead to increased efficiency and cost reduction across the business network. The features that make blockchain trusted for business include:

Consensus, because all parties must agree to network verified transactions.

Immutability, because anything written on the ledger cannot be altered.

Provenance, because there are records of where each asset has been.

Privacy, because permissions and identity ensure appropriate visibility of transactions.

The Idea of decentralization and distributed shared ledger

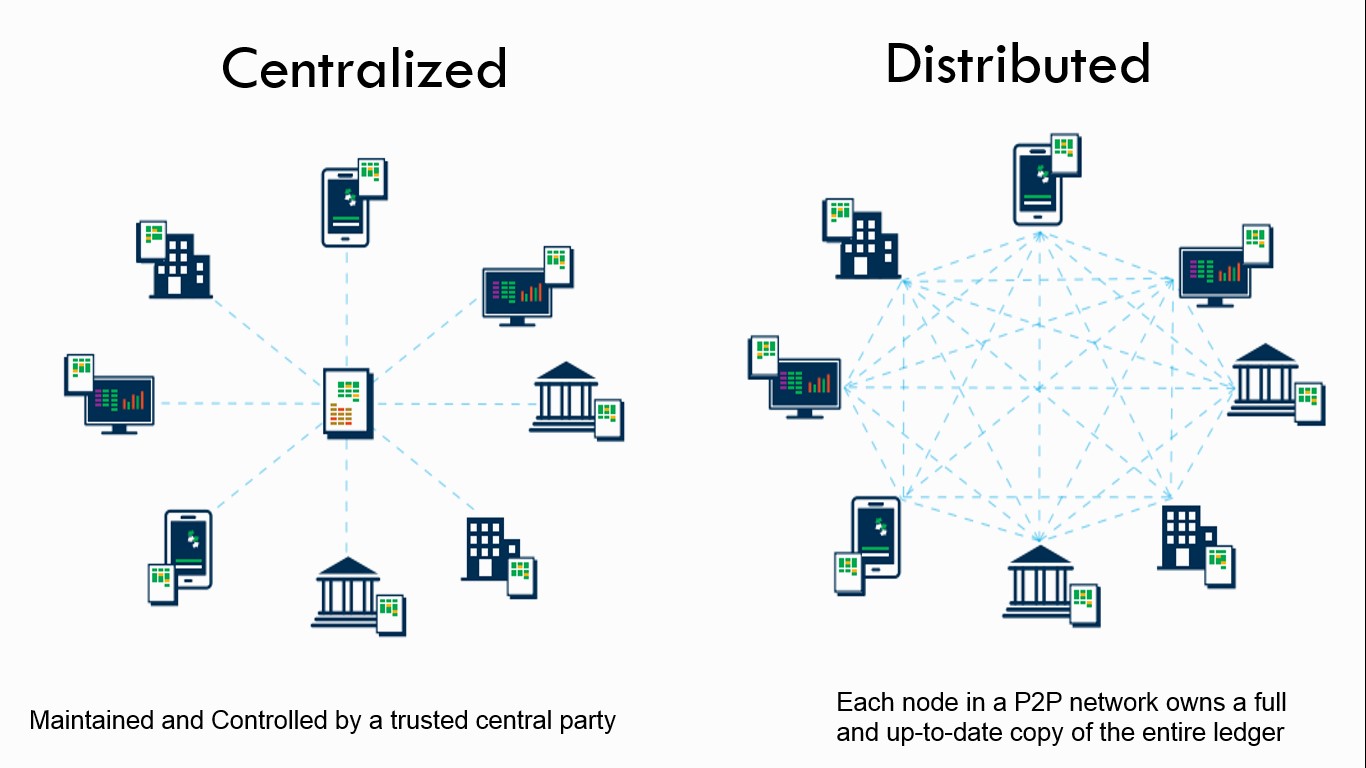

It’s important to understand that there is no single “blockchain” in computing much like there is no single “cloud”; rather, a blockchain is a peer-to-peer network with a distributed ledger that’s created by running the same software on many different computers.

In conventional system, several businesses rely on a centralized service model where data is stored or processed by a single entity. Think of popular social media services where user data is stored in central databases: users are solely reliant on the social media service for the integrity and longevity of their data. What happens if the service ceases operations, experiences a data breach, or inexplicably removes user content? By serializing certain data and storing it as transactions on a public blockchain instead of in a traditional centralized database, risks of malicious data tampering could be greatly reduced.

How blockchain works

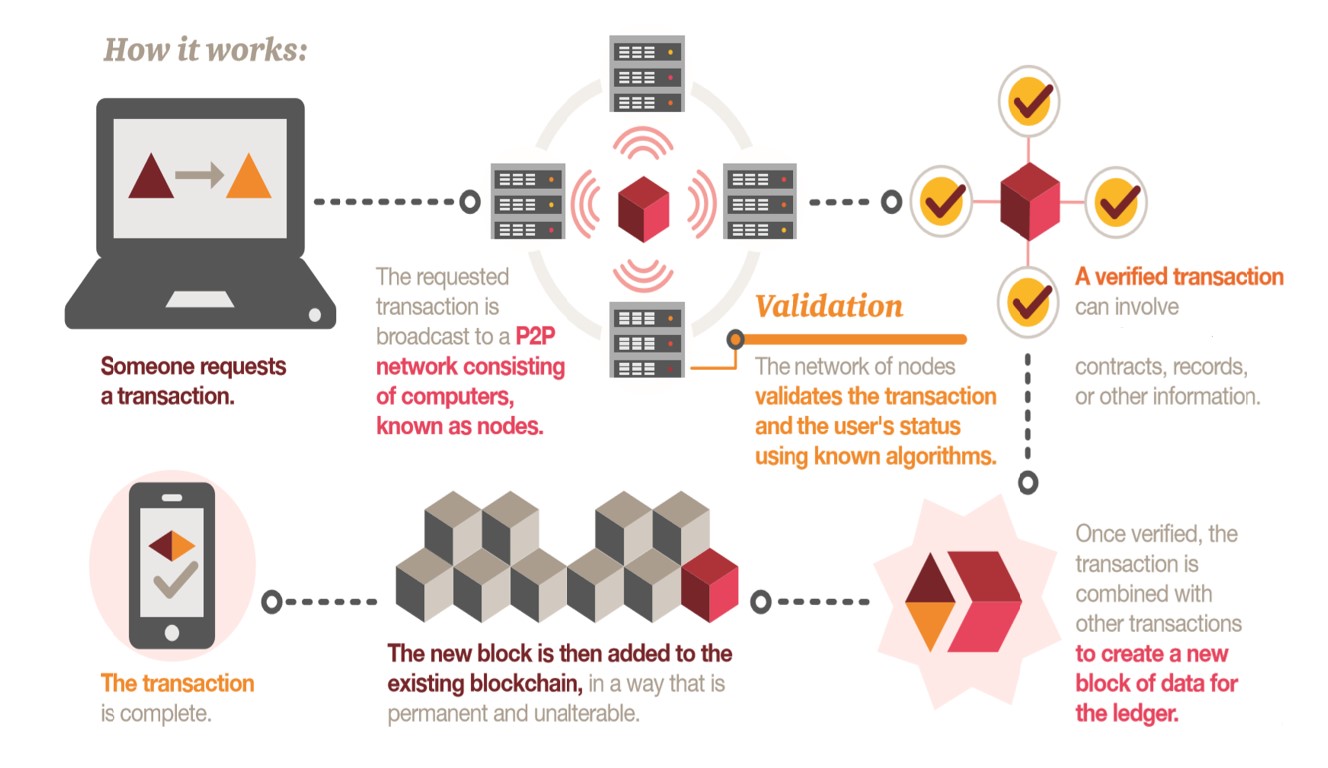

A blockchain is, well, a chain of blocks. It’s a method for sharing a record of an online transaction in a secure and trustworthy way that allows both parties to have a copy of that record without either party having to maintain that record.

Most digital transactions have a middleman, like a bank that verifies Party A has the funds and has duly transferred them to Party B in a trusted fashion. The blockchain allows you to skip the bank and transfer money, information, or other services directly to another entity over the internet in a method that both parties can trust. In blockchain network, the requested transaction is broadcasted to p2p network consisting of computers known as nodes, then the networks of nodes validate the transaction. Once verified the transaction is combined with other transactions to create a new block of data for the ledger. The new block is then added to the existing blockchain in way that is permanent and unalterable and the whole transaction is completed.

Smart Contract

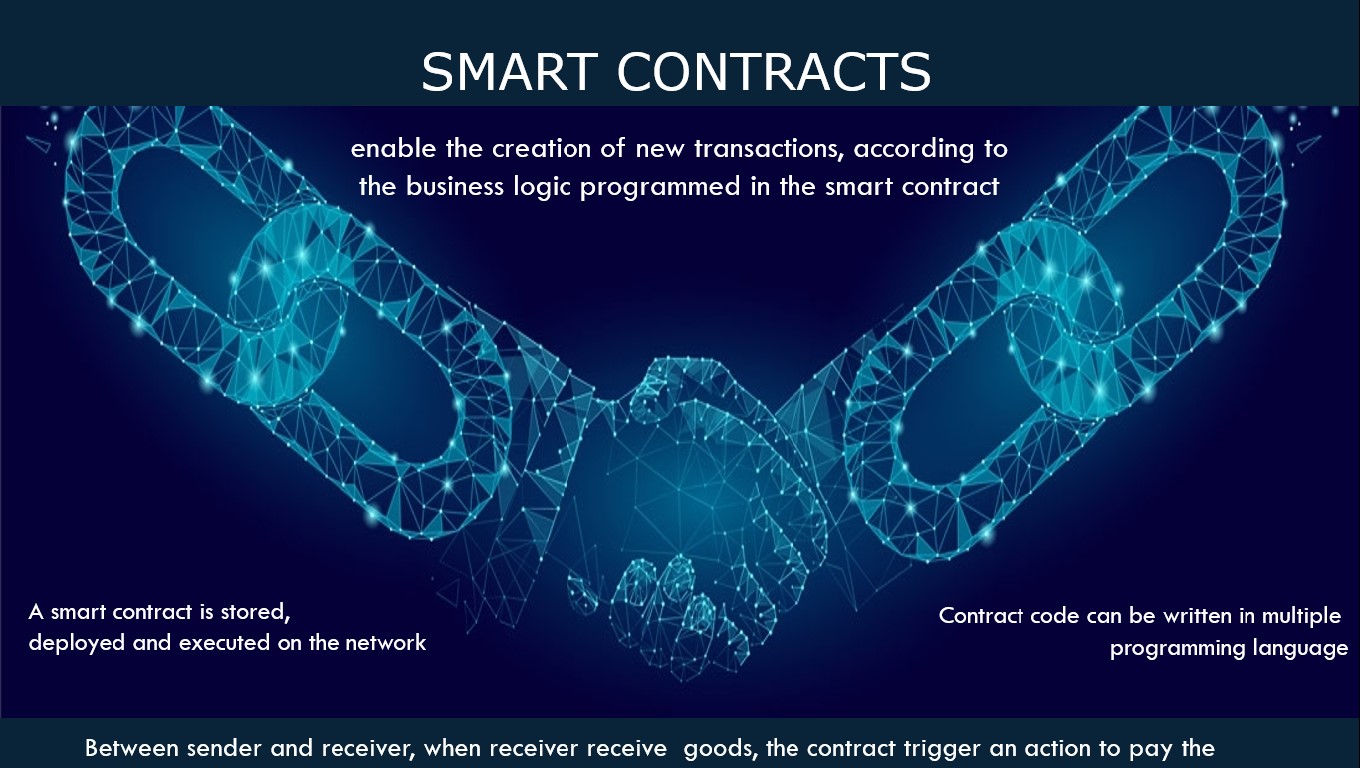

A smart contract is a self-executing contract with the terms of the agreement between buyer and seller being directly written into lines of code. The code and the agreements contained therein exist across a distributed, decentralized blockchain network. The code controls the execution, and transactions are trackable and irreversible. Smart contracts permit trusted transactions and agreements to be carried out among disparate, anonymous parties without the need for a central authority, legal system, or external enforcement mechanism

Blockchain Use Cases

Payments in Banking & Finance

Blockchain technology can be used to decrease the cost of international transfers by reducing the need for banks to manually settle transactions. And while that’s something Santander isn’t able to deliver using existing payment rails, it could potentially do so using a blockchain-based system

Trade Finance

The transaction of a letter of credit — a document that guarantees that the seller will be paid, and that the buyer will not have to make a payment until the goods are received. Executing a letter of credit is usually a slow, paper-based process, but blockchain could able to execute a deal in few hours that would usually take a week to complete. This could prove very significant, as the global trade finance sector is worth an estimated $10 trillion per year. blockchain could streamline trade finance deals, and highlights a concrete use case for the technology in financial services.

Regulatory Compliance and Audit

The extremely secure nature of blockchain makes it rather useful for accounting and audit because it significantly decreases the possibility of errors and ensures the integrity of the records. On top of this, no one can alter the account records once they are locked in using blockchain tech, not even the record owners.

Money Laundering Protection

The encryption that is so integral to blockchain makes it exceedingly helpful in combating money laundering. The underlying technology empowers record keeping, which supports “Know Your Customer (KYC),” the process through which a business identifies and verifies the identity of its clients.

Insurance

Arguably the greatest blockchain application for insurance is through smart contracts. Such contracts powered by blockchain could allow customers and insurers to manage claims in a truly transparent and secure manner. All contracts and claims could be recorded on the blockchain and validated by the network, which would eliminate invalid claims. For example, the blockchain would reject multiple claims on the same accident.

Supply Chain Management

Blockchain’s immutable ledger makes it well suited to tasks such as tracking goods as they move and change hands in the supply chain. Using a blockchain opens up several options for companies transporting these goods. Entries on a blockchain can be used to queue up events with a supply chain (allocating goods newly arrived at a port to different shipping containers, for example.

Healthcare

Health data that’s suitable for blockchain would include general information like age, gender, and potentially basic medical history data like immunization history or vital signs. None of this should be able to identify any particular patient, which is what allows it to be stored on a shared blockchain that can be accessed by numerous individuals without undue privacy concerns. As specialized connected medical devices become more common and increasingly linked to a person’s health record, blockchain can connect those devices with that record. Devices will be able to store the data that they generate on a health care blockchain that can append that data to a person’s medical record. A key issue facing connected medical devices is the siloing of the data they generate — blockchain can be the link that bridges those silos.

Real Estate

For the frequent movement of real state property by homeowners and byer ith such movement, blockchain could certainly be of use in the real estate market. It would expedite home sales by quickly verifying finances, would reduce fraud thanks to its encryption, and would offer transparency throughout the entire selling and purchasing process.

Record Management

National and local governments are responsible for maintaining individuals’ records such as birth and death dates, marital status, or property transfers. Yet managing this data can be difficult, and to this day some of these records only exist in paper form. And sometimes, citizens have to physically go to their local government offices to make changes, which is time-consuming, unnecessary, and frustrating. Blockchain technology can simplify this record keeping and make them far more secure.

Identity Management

Proponents of using blockchain tech for identity management claim that with enough information on the blockchain, people would only need to provide the bare minimum (date of birth, for example) to prove their identities.

Internet of Things (IoT)

Blockchain is poised to transform practices in a number of IoT sectors, including:

The supply chain: Tracking the location of goods as they are shipped, and ensuring that they stay within specified conditions.

Asset tracking: Monitoring assets and machinery to record activity and output as an alternative to cloud solutions.

Health care: Enabling logging and sharing of medical data between numerous stakeholders with versatile permissioning, directly holding some data while offering encrypted links to other information.

Ref:

https://blockgeeks.com/guides/what-is-blockchain-technology/

http://www.businessinsider.com/blockchain-technology-applications-use-cases-2017-9